Building credibility and trust in the delivery of their service controls and procedures is a goal of service organizations’ (SOC) reporting. While SOC 3 reports assist in streamlining audit procedures, SOC 1 and 2 audit reports assist consumers in complying with audit demands from outside accounting firms. The efficacy or lack thereof of these controls influences the user organization’s trustworthiness, financial statements, and stability. SOC 1 and 2 reports give transparency of the precise controls employed by service organizations. Each client has distinct expectations from service organizations about various facets of their operations, and SOC reports are created to satisfy these expectations. Read this article on soc 1 vs soc 2

A SOC 1 Report

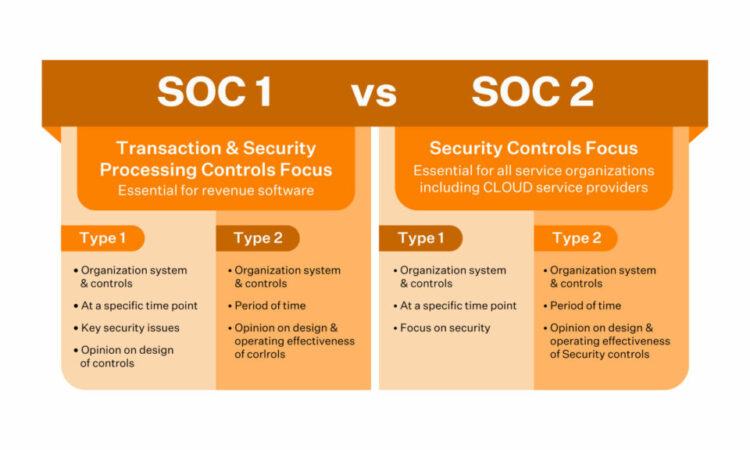

The SOC 1 report, formerly referred to as the SSAE 18, has a financial focus and includes the controls of the service organization that are important to an audit of an end-user entity’s (customer’s) financial statements. Information technology and business processes are both relevant to control objectives.

The overview of a service organization’s controls and the appropriateness of how those measures are intended to fulfill the control goals as of a given date are the main topics of a SOC 1 – Type I audit report.

The views in a SOC 1 Type II audit report are identical to those in a Type I audit report, but they also provide an assessment of the operating effectiveness in achieving associated control goals over a certain period. SOC 1 audit reports are only available to user auditors, user entities, and the operational management of the services organization

A SOC 2 Report

SSAE 18 was the former name for the SOC 2 report. It was developed in part as a result of the development of cloud computing and business function outsourcing to service providers.

In the SOC reports, these are referred to as user entities. A need for a guarantee of the confidentiality and privacy of the information handled by the system has arisen due to liability concerns.

SOC 2 refers to a report on the controls of a service organization’s availability, security, processing integrity, confidentiality, and privacy.

The report discusses the operations and compliance controls in connection with its services, operations, and compliance as described by the AICPA’s Trust Services standards. Any one of the five Trust Service principles may be the topic of a SOC 2 report, and a service company may select either a Type I or Type II SOC 2 certification.

The outcomes of the service auditor’s examination of controls are fully described in a SOC 2 report. This report’s usage is typically limited.

How Do SOC 1 and SOC 2 Differ From One Another?

The focus is different, although SOC 1 reports concentrate on financial controls, SOC 2 reports provide additional attention to availability, security, processing integrity, confidentiality, and privacy.

{kind=link}